MADRID, 8 Mar. (EUROPA PRESS) -

The Ibex 35 closed the week with a rise of 2.39%, to 10,305.7 points, a few days marked by the monetary policy meeting of the European Central Bank (ECB) and by the volatility in the Grifols price.

The selective has lost 0.13% in this Friday's session, although it has held the level of 10,300 integers. Even so, the index is trading at levels not seen in the Spanish stock market since February 2018.

"The Spanish stock market registered new annual highs driven by the optimism aroused by the latest appearances by Christine Lagarde and Jerome Powell. Although both continue to condition the decision to cut rates to the evolution of the next data, investors began to discount the possibility of for this to happen in the month of June," said XTB analyst Joaquín Robles.

On Wednesday, the Chairman of the United States Federal Reserve (Fed), Jerome Powell, stated that progress in returning inflation to the 2% target is not "certain", thus underscoring the need for more data than confirm the convergence of prices with said 2% before undertaking cuts in interest rates.

On Thursday, ECB President Christine Lagarde indicated that the disinflation process offers greater confidence to members of the authority's Governing Council, adding that, while there will be a little more information in April, there will be "much more in June".

In this sense, the governors of a handful of central banks of euro zone countries and, therefore, members of the Governing Council of the European Central Bank (ECB), led by the presidents of the Bundesbank and the Bank of France, have supported this Friday the possibility that the first interest rate reduction will arrive before the summer, ensuring that it will be an issue to be discussed at the meetings in April or more likely June.

The week has also been marked because the bearish fund Gotham City Research has published a new report on Grifols, in which it accuses the company of making loans in a non-transparent manner to the 'family office' owned by the Grifols family, Scranton, through from Haema and BPC. In addition, he has criticized that the interest that Scranton pays on these loans to Haema and BPC, two firms of which Scranton has ownership, is greater than the interest that these companies pay to Grifols for the money they receive.

The price of the blood products firm has recovered part of its fall this Friday after the auditor KPMG has supported the company's accounts without any reservation.

In the business field, it is also notable that the Hungarian group Ganz-Mavag (Magyar Vagon) officially presented this Thursday at the close of the market before the National Securities Market Commission (CNMV) a public offer for the acquisition of shares (OPA) to become with 100% of Talgo for 619 million euros.

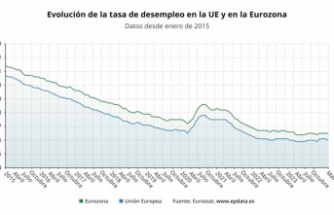

Under the macroeconomic umbrella, this Friday it was published that the gross domestic product (GDP) of the eurozone finally avoided entering into a technical recession - which implies two consecutive quarters of decline in activity - after in the fourth quarter of 2023 the economy will stagnate, after the contraction of 0.1% in the previous three months, as confirmed this Friday by Eurostat.

In this context, Grifols has been the most notable value this Friday, rising 19.7% and moving away from the lows since 2012 that it had marked with the new Gotham 'coup'. Behind them were Colonial (2.77%), Aena (2.31%), Merlin (1.81%), Bankinter (1.14%), Fluidra (0.54%) and Meliá (0.53). %).

On the negative side were Acciona Energía (-3.97%), Solaria (-3.40%), Acciona (-2.69%), Naturgy (-2.11%), Endesa (-1.83% ), Rovi (-1.58%), Sacyr (-1.19%).

In the rest of the European stock markets, only Paris closed positive (0.15%). London has fallen 0.43%; Frankfurt, 0.16%; and Milan, 0.04%.

The barrel of Brent experienced a decrease of 0.98% at the close of the European trading session, to $82.12, while West Texas Intermediate (WTI) fell 1.24%, to $77.94.

In the debt market, the yield on the Spanish bond with a 10-year maturity closed the week at 3.08%, from 3.121% on Thursday. In this way, the risk premium against German debt has fallen to 81.3 basis points, two tenths less than on Thursday.

In the foreign exchange market, the euro was trading practically flat against the dollar compared to the previous day, trading at an exchange rate of 1.0945 'greenbacks' for each unit of the community currency.

Next week will be marked by the publication of various macro data. On Monday, Japan's GDP and Spain's retail sales will be released, while on Tuesday it will be the turn of unemployment in the United Kingdom and inflation in Germany, as well as the monthly OPEC report and the CPI in the United States.

On Wednesday, the United Kingdom will publish its GDP data, while eurozone industrial production will be known. On Thursday it will be the turn of Spain's inflation.

The week will conclude with inflation data from France and Italy, as well as with the BBVA and Mapfre shareholder meetings.